_large.jpg)

The textile and apparel industry (T&A) is undergoing a fundamental shift, and this disruption is likely to become the ‘new normal.’ Several structural changes—geopolitical tensions, nearshoring, sustainability regulations, and digitalization—are reshaping trade and investment patterns.

Here are three key trends I anticipate over the next five years:

1. Regionalization & Nearshoring

The days of full reliance on long, globalized supply chains are fading. Rising geopolitical risks, high shipping costs, and demand for faster turnaround times are pushing brands to source closer to consumer markets.

Expect an increase in investments in nearshoring hubs like Mexico (for the U.S.), Türkiye (for Europe), and North Africa. However, this won’t entirely replace Asian suppliers but will lead to a more diversified sourcing strategy.

Join our group

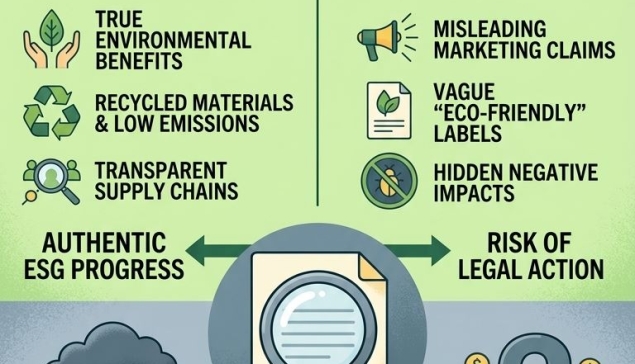

2. Sustainability-Driven Trade Policies

Regulations like the EU’s Carbon Border Adjustment Mechanism (CBAM) and Ecodesign Directive will impact trade flows by penalizing high-carbon and non-compliant products.

Supply chain transparency requirements (e.g., Germany’s Supply Chain Act) will make compliance a key investment priority.

Recycling and circularity initiatives will push new investment into textile-to-textile recycling and material innovation.

Join our community

3. Digitization & AI in Supply Chains

AI-driven demand forecasting, automated production, and real-time tracking will become standard, improving efficiency and reducing waste.

Blockchain and digital product passports will facilitate traceability, helping companies comply with new regulations and differentiate products.

Investments in smart factories, 3D sampling, and automated sewing technology will accelerate, shifting cost advantages away from purely low-wage labor markets.

CREDITS: Cem Altan | President | International Apparel Federation (IAF).